ALTERNATIVE BUSINESS FINANCE PRODUCTS

When businesses, whether sole traders, large corporations, or public sector entities, seek to invest in tangible assets, they often require a secure and cost-effective financing solution. Asset Finance is the third most common source of business funding, following bank overdrafts and loans.

The two primary forms of Asset Finance are Hire Purchase and Leasing.

Hire Purchase (HP)

-

Instead of paying a large lump sum upfront, Hire Purchase allows You to spread the cost of an asset over a period ranging from 1 to over 10 years, depending on the asset and your financial situation.

-

You gain ownership of the asset after making the final payment, including the "option to purchase fee."

-

During the payment term, the lender retains ownership, effectively leasing the asset to You.

-

Hire Purchase offers a straightforward and flexible financing solution.

-

Interest rates can be either fixed or variable.

-

You can tailor the repayment term and deposit to match Your budget and financial needs.

Disadvantages of Hire Purchase:

-

You must repay the full amount according to the agreed schedule. Failure to do so may result in asset repossession and a negative impact on Your credit rating.

-

Due to interest charges, the total cost of the asset will be higher than its purchase price.

-

Ownership is only transferred once all payments, including the option to purchase fee, are made.

-

Assets may depreciate faster than the repayment period, potentially leaving You with a liability exceeding the asset's value.

-

If you choose an unregulated fixed-rate Hire Purchase agreement, You remain responsible for the outstanding balance and interest.

-

Early settlement may result in higher costs, so it is crucial to review the lender's "Early Termination Charges" outlined in the finance agreement.

Leasing

-

With leasing, a commercial agreement is made where the leasing company (lessor) purchases and owns the asset, while You (the lessee) pay regular rentals to use it. At the end of the contract, You typically have options to extend the lease, return the asset, or purchase it through an unrelated third party.

-

The two main types of leases are Finance Lease and Operating Lease.

Finance Lease

-

The lessor retains ownership throughout the lease term, which generally spans the full economic life of the asset.

-

At the end of the term, You may have the option to continue leasing at a reduced rate (often referred to as a ‘peppercorn’ rate).

-

Since You do not own the asset, You cannot sell it during the lease period.

-

The lessor can claim writing-down allowances and may pass these benefits to You through lower rental costs.

Operating Lease

-

The lease term is shorter than the asset’s full economic life, and You are not responsible for financing its total value.

-

The lessor assumes the risk of the asset’s residual value at the end of the lease.

-

Operating leases are commonly used for assets with strong resale value, such as transportation equipment.

-

This option is ideal for companies that frequently update or replace equipment without the need for ownership.

-

In motor finance, contract hire is the most common type of operating lease, particularly or vehicle fleets.

Disadvantages of Leasing:

-

Lease agreements require fixed rental payments. If You experience financial difficulties and cannot meet these obligations, You risk losing the asset and damaging Your credit rating.

-

Since You are not the asset’s legal owner, You cannot claim writing-down allowances.

-

Interest rates are determined based on risk. Businesses with lower credit ratings or operating in high-risk industries may face higher costs.

-

While leasing offers flexibility, early contract termination usually incurs penalties.

-

Lease agreements often include conditions regarding asset maintenance and return requirements. Reviewing these terms is essential to avoid unexpected costs.

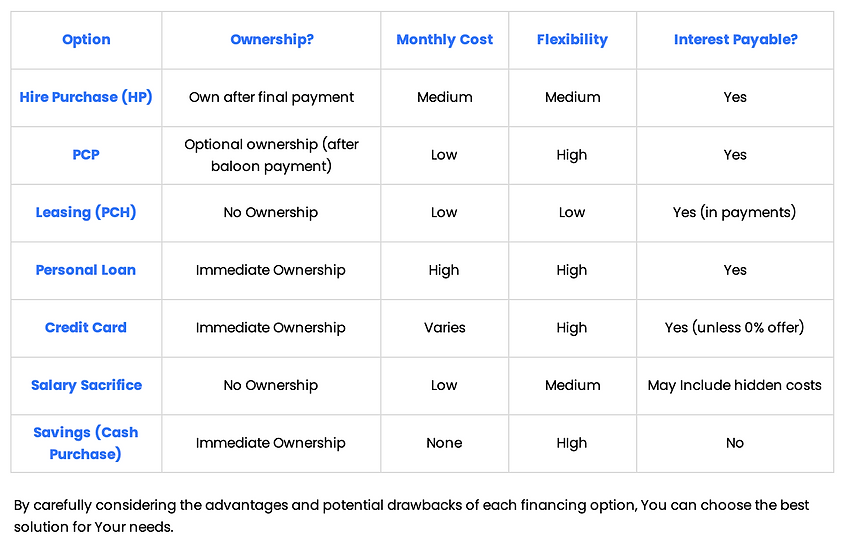

By carefully considering the advantages and potential drawbacks of each financing option,

businesses can choose the best asset finance solution for their needs.

Alternative Personal Car Finance Products

If You are looking at alternatives to finance a car, there are many options available. Each has its

own advantages and disadvantages, depending on Your circumstances, budget, and priorities

(e.g., ownership, flexibility, or lower monthly payments).

Hire Purchase (HP)

How it works : The lender assesses Your credit score, income, and affordability to decide how

much You can borrow and at what interest rate. The lender then pays for the vehicle and You

repay the lender over an agreed term at an agreed interest rate.

Advantages:

-

Once you make the final payment (including the Option to Purchase fee), the car is yours.

-

Rather than paying a large lump sum upfront, you spread the cost over a fixed period (typically 1 to 5 years).

-

Most HP agreements offer fixed interest rates, meaning your monthly payment stays the same, even if interest rates rise.

-

You can choose how much deposit to put down (subject to minimum requirements). Larger deposits reduce monthly payments.

-

Because the car itself acts as security for the lender, HP can be easier to get approved for compared to unsecured personal loans.

-

Unlike PCP or leasing, there are no mileage limits with HP. You’re free to drive as much as you like.

Disadvantages:

-

Compared to PCP or leasing, monthly payments tend to be higher because you’re paying off the full cost of the car.

-

The lender legally owns the car until you make the final payment — so you can’t sell or modify the car until then.

-

If you miss payments, the lender can repossess the car because they technically own it until you complete the agreement.

-

Due to interest charges, you end up paying more overall than if you had bought the car outright with cash.

-

If you want to pay off the agreement early, you could face early repayment penalties, although these vary by lender.

-

If the car loses value faster than expected (which often happens with new cars), you might owe more than the car is worth if you want to settle the agreement early.

Personal Contract Purchase (PCP)

How it works : You pay lower monthly payments over a set term (usually 2-4 years), with a large optional final payment (called a balloon payment) if You want to own the car at the end. Otherwise, You can return the car or trade it in for a new one.

Advantages:

-

Lower monthly payments than HP.

-

Flexibility at the end: You can return, buy, or upgrade to a new car.

-

Good for people who like to change cars frequently.

-

Sometimes includes manufacturer incentives like servicing deals.

Disadvantages:

-

You don’t automatically own the car (ownership only comes after paying the balloon payment).

-

Balloon payment can be expensive if You choose to keep the car.

-

Mileage limits apply – exceeding them incurs charges.

-

You may also face fees for excessive wear and tear when returning the car.

Leasing (Personal Contract Hire - PCH)

How it works: This is essentially long-term car rental. You make fixed monthly payments to rent

the car, then return it at the end of the lease period (usually 2-4 years).

Advantages:

-

Monthly payments are often lower than both HP and PCP.

-

No worries about depreciation or resale.

-

Sometimes includes servicing/maintenance packages.

Disadvantages:

-

You never own the car.

-

Strict mileage limits with penalties for exceeding them.

-

Termination charges apply if You end the lease early.

-

Car must be returned in good condition, or You will face additional charges.

Personal Loan

How it works: You borrow money from a bank, or alternative lender, then use it to buy the car

outright.

Advantages:

-

You own the car immediately.

-

No mileage restrictions.

-

Can be cheaper if You qualify for a low-interest loan.

-

Flexibility to sell or modify the car at any time.

Disadvantages:

-

Approval depends on Your credit score and financial history.

-

Higher monthly payments than PCP or leasing.

-

Interest rates may be higher than secured car finance options like HP.

Credit Card (if buying a cheaper car)

How it works: For lower-cost vehicles, you could use a credit card to pay either the whole price

or part of it.

Advantages:

-

Quick and easy if you have an existing card.

-

Possible to benefit from 0% purchase deals.

-

Section 75 protection (in the UK) if something goes wrong with the purchase.

Disadvantages:

-

High-interest rates if not paid off quickly.

-

Credit limits might not cover the full purchase.

-

Risk of negatively affecting your credit score if you borrow too much of your available limit.

Salary Sacrifice (if available through your employer)

How it works: Some employers offer car schemes where payments are taken directly from your

salary before tax.

Advantages:

-

Tax-efficient, reducing your taxable income.

-

Often includes insurance, servicing, and maintenance.

-

No credit checks, as it’s part of your employment benefits.

Disadvantages:

-

Only available through participating employers.

-

You lose the car if you leave the job.

-

May affect other workplace benefits (like pension contributions).

Savings (Paying Cash)

How it works: If you have savings, you could simply buy the car outright.

Advantages:

-

No interest or fees.

-

Full ownership from day one.

-

No contracts or restrictions.

Disadvantages:

-

Large upfront cost.

-

Ties up your savings, which could be used elsewhere (e.g., emergencies or investments).